Real Estate

Virginia home prices still climbing, but cooling market brings moderation

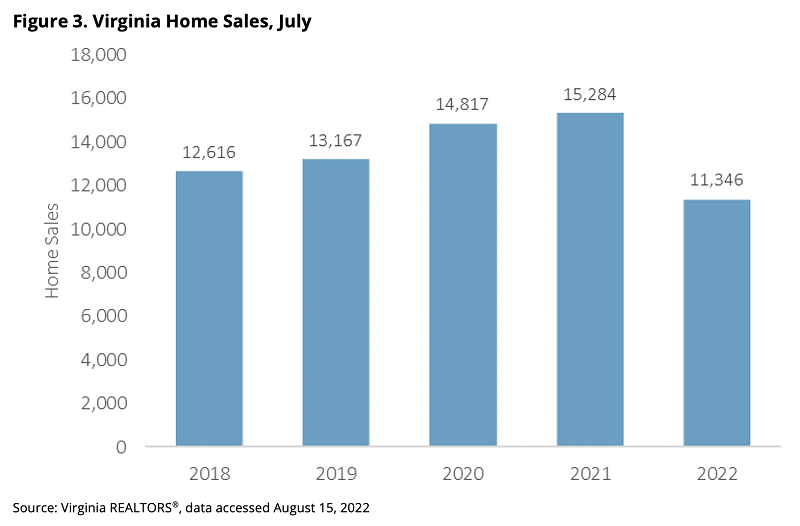

According to the July 2022 Virginia Home Sales Report released by Virginia REALTORS®, there were 11,346 homes sold in Virginia in July 2022. This is nearly 26% fewer than July 2021, the sharpest year-over-year drop in more than seven years. Overall, sales activity has been moderating from last year’s level in Virginia since last fall.

While total sales activity continues to slow down considerably, home prices in the market are still climbing. At $385,000, the July median sales price in Virginia rose nearly 7% from a year ago, a gain of $25,000.

While the price trajectory is still creeping upward, indicators suggest that the upward pressure is easing. “In most price segments, homes are still selling for more than the listing price, on average. However, that ratio has been inching down for several months,” says Virginia REALTORS® 2022 President Denise Ramey. “We aren’t seeing quite as many bidding wars as we did just a few months ago, and we expect price growth will moderate even more as the market activity continues to cool.” The average sold-to-ask price ratio across the state was 101.2%, down from 102.4% last month (June 2022), and down from 101.8% last July.

While Virginia’s statewide inventory of homes still remains low, in many local housing markets around the commonwealth, the supply of active listings is growing. About half of all counties and independent cities in the state had more active listings at the end of July compared to a year ago.

“The expanding supply is good news for buyers in the market,” says Virginia REALTORS® Chief Economist Ryan Price. “Buyers’ purchasing power has been impacted by elevated inflation and rising mortgage rates. The slowdown in sales activity we’ve seen in many areas of the state is resulting in a buildup of available homes.”

The Virginia Home Sales Report is published by Virginia REALTORS®. Click here to view the full July 2022 Virginia Home Sales Report.

Front Royal Cardinals Host Purcellville Cannons Sunday, June 21 at Bing Crosby Stadium

America 250: The Smithsonian Comes to You

Regular Maintenance Keeps Electric Fences Working Properly

Virginia House, Senate to Meet Monday as Budget Deadline Inches Closer

Louise Elizabeth Mills (1937 – 2026)

Suspected Drug Trafficker Arrested After Interstate Chase Through Warren and Shenandoah Counties

Business Growth Series: Why Customers Choose Businesses That Show Energy and Confidence

Small Reactors, Big Ambitions

Virginia Unveils East Coast’s Deepest Shipping Channel at Port of Virginia

Warren County Election Staff Earn Federal Election Administration Certification

Weeding Through the True Cost of Building a Cannabis Market to Balance the Budget

Commentary: Four Virginia Counties Will Pump Almost 20 Million Gallons of Water a Day to Amazon… Cause for Concern?

What Parents and Grandparents Need to Know About Child Tax Credits in 2026

Choosing the Right Garden Swing Starts with Space, Style and Material

Front Royal Cardinals Return Home Friday, June 19 to Face Strasburg Express

Town Planning Commissioners Recommend Denial of Proposed Junkyard

Lawmakers Demand Interior Department Explain Use of Park Visitor Fees

What Not to Say in Your First Weeks on the Job

Some Former Felons, Eligible to Vote This Summer, are in Registration Limbo

State Code Allows Front Royal and Warren County to Ban Data Centers

Shelby Gene Bailey (1941 – 2026)

The No-Miss Father’s Day Dinner

Small Changes Can Improve a Vehicle’s Aerodynamics and Fuel Efficiency

Blue Ridge Wildlife Center Patient of the Week: Central Ratsnake(s)